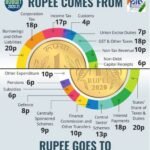

BUDGET 2020: Direct Tax Proposals

BUDGET 2020: Direct Tax Proposals

To stimulate growth, simplify tax structure, bring ease of compliance, and reduce litigations. ·

Personal Income Tax:

o Significant relief to middle class taxpayers.

o New and simplified personal income tax regime proposed:

| Taxable Income Slab (Rs.) | Existing tax rates | New tax rates |

| 0-2.5 Lakh | Exempt | Exempt |

| 2.5-5 Lakh | 5% | 5% |

| 5-7.5 Lakh | 20% | 10% |

| 7.5-10 Lakh | 20% | 15% |

| 10-12.5 Lakh | 30% | 20% |

| 12.5-15 Lakh | 30% | 25% |

| Above 15 Lakh | 30% | 30% |

o Around 70 of the existing exemptions and deductions (more than 100) to be removed in the new simplified regime.

o Remaining exemptions and deductions to be reviewed and rationalised in coming years.

o New tax regime to be optional – an individual may continue to pay tax as per the old regime and avail deductions and exemptions.

o Measures to pre-fill the income tax return initiated so that an individual who opts for the new regime gets pre-filled income tax returns and would need no assistance from an expert to pay income tax.

o New regime to entail estimated revenue forgone of Rs. 40,000 crore per year.

- Corporate Tax:

o Tax rate of 15% extended to new electricity generation companies.

o Indian corporate tax rates now amongst the lowest in the world.

- Dividend Distribution Tax (DDT):

o DDT removed making India a more attractive investment destination.

o Deduction to be allowed for dividend received by holding company from its subsidiary. o Rs. 25,000 crore estimated annual revenue forgone.

- Start-ups:

o Start-ups with turnover up to Rs. 100 crore to enjoy 100% deduction for 3 consecutive assessment years out of 10 years.

o Tax payment on ESOPs deferred.

- MSMEs to boost less-cash economy:

o Turnover threshold for audit increased to Rs. 5 crore from Rs. 1 crore for businesses carrying out less than 5% business transactions in cash.

- Cooperatives:

o Parity brought between cooperatives and corporate sector.

o Option to cooperative societies to be taxed at 22% + 10% surcharge and 4% cess with no exemption/deductions.

o Cooperative societies exempted from Alternate Minimum Tax (AMT) just like Companies are exempted from the Minimum Alternate Tax (MAT).

- Tax concession for foreign investments:

100% tax exemption to the interest, dividend and capital gains income on investment made in infrastructure and priority sectors before 31st March, 2024 with a minimum lock-in period of 3 years by the Sovereign Wealth Fund of foreign governments.

- Affordable housing:

o Additional deduction up to Rs. 1.5 lakhs for interest paid on loans taken for an affordable house extended till 31st March, 2021.

o Date of approval of affordable housing projects for availing tax holiday on profits earned by developers extended till 31st March, 2021.

Tax Facilitation Measures

- Instant PAN to be allotted online through Aadhaar.

- ‘Vivad Se Vishwas’ scheme, with a deadline of 30th June, 2020, to reduce litigations in direct taxes: o Waiver of interest and penalty – only disputed taxes to be paid for payments till 31st March, 2020. o Additional amount to be paid if availed after 31st March, 2020.

o Benefits to taxpayers in whose cases appeals are pending at any level.

- Faceless appeals to be enabled by amending the Income Tax Act.

- For charity institutions:

o Pre-filling in return through information of donations furnished by the done. o Process of registration to be made completely electronic.

o Unique registration number (URN) to be issued to all new and existing charity institutions. o Provisional registration to be allowed for new charity institutions for three years.

o CBDT to adopt a Taxpayers’ Charter.

- Losses of merged banks: o Amendments proposed to the Income-tax Act to ensure that entities benefit from unabsorbed losses and depreciation of the amalgamating entities.

0 Comments